Buried under the ridiculous complexity of modern economics is the straightforward concept of supply and demand. Sadly, it’s submerged under a mountain of mathematical models and equations designed to confuse and impress those who don’t study economics. Who wants to think about common sense explanations when you can plug some numbers into a super-cool “multivariate regression model” and sound so much smarter? Economists do, that’s who.

Economists are like “The Great Oz”, employing math to garner awe from those too distracted to see their analytical mediocrity. To be fair, it’s hard to justify the tens of millions of dollars the Federal Reserve spends each year on salaries if the analysis is attainable by a 7th grader with basic logical skills. You’re supposed to focus on the smoke and mirrors…on the booming voices from theEccles Building. As Oz said,“Pay no attention to the man behind the curtain.”

Who’s the man?

Not Jerome Powell. Of course, the Fed chairman gets all the headlines and media coverage. His speeches are blasted across the financial news wire, and the fed meeting minutes are thoroughly exegeted to obtain every nuance. We’re supposed to believe that the Fed is at the center of the financial world, and their models will show us where things go from here.

As the voices of our financial Oz continue to declare their “model-driven” insights with authority, we plebians will quickly forget how poorly their predictions have fared in the past. We’ll forget that in September 2021, the Fed expected to hike rates once or twice the following year. By the end of 2022, however, the Fed had hiked an equivalent of 17 times. We’ll forget that in March 2018, the Fed expected the Fed Funds Rate to be 3.4% by the end of 2020, but instead began cutting in mid-2019 and ended up at 0%. These are two gigantic misses in just the past 5 years. And like a DeLorean, the Fed’s track record doesn’t get any better by going back in time.

But if the Fed isn’t the man, who is? The man isn’t so much a person as it is the people that make up the economy. The man has, as Adam Smith once famously put it, invisible hands that guide the direction of the market economy. Certainly, government policy and central bank meddling can influence the market, but the invisible hands eventually get their way. Even in the Soviet Union, the strong arms of a socialist government eventually succumbed to the limitations of reality imposed on it by the underground market economy.

But let’s not give the Fed too much credit. It isn’t that the Fed sometimes gets it wrong, or that their models are incomplete. Rather, the Fed is almost always wrong because they rely on models that – at best – describe the past. Economists assume that a model that describes the past provides some predictive power, but it doesn’t. And the history of the Fed “revising” (i.e., completely changing) their projections proves that it doesn’t.

If not models, then what?

As Smith put it, even when a business owner is concerned with “only his own gain…he is led by an Invisible Hand to promote an end which was no part of his intention.” Every day millions of decisions are made by business owners and consumers, acting in their own self-interest. Note, I’m not saying they are selfish (although I’m sure some are). Rather, I’m saying that they act to accomplish something that they desire. And that’s not necessarily selfish, per se. Taking action to accomplish a goal is why any of us do anything. But Smith recognized that the invisible hand guides these actors to do things that benefit others – even when they have no intention of doing so.

These interactions produce money prices, which are the consequence of supply and demand for scarce resources. Money prices inform us how and where we and others are spending our money, and our decisions help to create new money prices all the time. It really is that simple. You can leave complex math models to the experts who are almost always wrong. Instead, focus on supply and demand to know where the economy is heading.

Having said all this, there is perhaps no commodity that can give us better insight into the underbelly of supply and demand in the economy, and where things are likely to head from here.

Black Gold

In the modern world oil exerts an enormous impact on the global economy. From prices at the pump, to diesel for trucks, to electric utility costs, the costs of oil-derived energy are a huge part of what makes the world economy go ‘round. The price of oil can go up or down for a variety of reasons, but it always boils down to supply and demand.

In 2023, the price of Crude oil ended the year essentially where it began, after falling nearly 40% in the second half of 2022.

This surprised many oil market analysts, who expected the price to remain well north of $100 per barrel after reaching $120 in June of 2022. Expectations were for supply to remain stable in 2023 while demand would pick up, largely due to China reopening after two years of COVID lockdowns. An increase in demand with stable supply would inevitably lead to rising price.

So why did the price of oil not increase? There are two possibilities. Supply could have increased more than expected, thus pushing prices lower. Except, that didn’t happen. In fact, supply was cut several times in 2023 by OPEC members, who wanted to – you guessed it – push prices higher! These cuts led to a fall in global supply of almost 6% - a massive decline which, to OPEC’s point, should have pushed prices higher.

In addition to the supply cuts, 2023 also saw the continued war in Ukraine, which means that embargoes on Russian oil and gas have continued to disrupt the flow of supply to the rest of the world. But it gets even worse on the supply front, as the war in Gaza and the general unrest in the Middle East (where OPEC is mostly located) added to supply constraints throughout 2023. And yet, prices remained well below expectations.

We don’t need a complex mathematical model to know why. It’s really quite simple: in the face of significantly falling supply, flat to lower prices means demand is falling. If it were stable or rising, as many analysts expected, prices would be going much higher. The fact that they have been flat for the past 12 months, and are down nearly 40% over the past 18, is a sign of falling demand. While falling demand could result from other factors (like innovation, for instance), there has been no revolutionary changes to industry in the past two months which would explain away the surprising lack of demand.

Further, the shape of the oil futures market suggests that demand is going to continue to be a problem. The futures curve has been in and out of something called “contango” all the way out to May of this year for a few months now. Without going into detail, contango typically occurs when demand is expected to remain below expectations. In other words, it means the oil market is expecting even lower prices going forward, despite the persistent and seemingly increasing supply problems.

While lower oil prices are a welcome sign for consumers at the gas pump, they indicate a weakening economy. Simply put, a lack of demand for oil is a tell-tale sign of recession.

The Importance of Corroboration

Like all narratives, they can sound plausible even if they’re completely wrong. This is one reason why looking for corroborating data points is so important. We can see the “weak economy” narrative showing up in other areas as well, such as:

- Global Shipping Costs: During the inflationary episode of 2021-2022, global container freight costs jumped from historical norms around $1000-$2000 per container to north of $10,000, due to (you guessed it!) both a lack of supply and increased demand. However, as supply chains have smoothed out expectations were for prices to moderate. Interestingly, they haven’t just moderated, they’ve plummeted 70-80%. Many shipping costs are back to or below their historic norms. In fact, the Baltic Dry Index, which is a volatile yet good barometer of global shipping costs, has plummeted 70% in the last two months. This occurred while Houthi Rebels are attacking the shipping lanes of the Red Sea, putting strain on supply and thus putting upward pressure on prices.

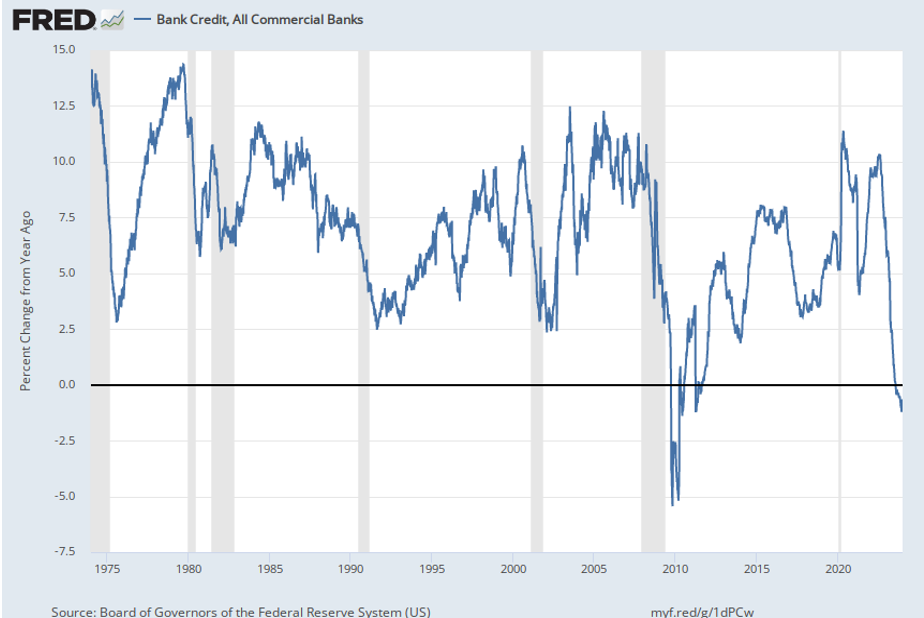

- Bank Credit: Demand for bank loans has been falling for well over a year now. This lack of demand has led to total bank credit contracting for only the third time in the past 50 years. The prior two times were during and immediately after the Great Financial Crisis.

- Commodities: From lumber to corn to wheat, commodity prices have fallen considerably over the past 18 months. The GSCI Commodity Index, for instance, remains over 30% below its most recent high in 2016, and far below its all-time high in 2008. All this despite continues geopolitical supply constraints and a lack of productivity increases.

- Lastly, the Inverted Yield Curve: The yield curve chart is supposed to look like the ascending half of a hill. Not a valley. When it looks like a valley, the entire financial system is seeing weakening growth and lower inflation on the horizon. Current levels of inversion are near historic extremes.

Conclusion

The next time you hear an economist suggesting that their model indicates this or that, don’t get distracted by the presentation. Instead, be reminded of Toto pulling the curtain back to reveal a senile old man speaking into a microphone.

Image from Wizard of Oz (1939).